Reducing tax liabilities requires smart planning. You can save significant money by making informed decisions. Firms have strategies to help you do this. First, they assess your financial situation. Then, they recommend actions for tax efficiency. This might include taking advantage of credits or deductions. They can also suggest retirement contributions or charitable giving. Each action reduces what you owe. Also, they keep up with tax law changes. This ensures you’re using every legal opportunity to save. Working with a professional like a tax return preparer in Carmel, NY can provide peace of mind. You get expert knowledge and guidance as they apply these strategies. Together, you can create a plan that works for you. This approach not only reduces your tax bill but also helps you keep more of your hard-earned money. Remember, every dollar saved is one you can invest back into your life or business.

Understanding Tax Strategies

Firms use various methods to help you manage taxes. Understanding these strategies can maximize your savings. One common approach is income deferral. By delaying income, you can potentially benefit from lower tax rates. This strategy is especially useful if you expect to be in a lower tax bracket in the future. Additionally, firms might recommend income shifting. This involves transferring income to family members in lower tax brackets.

Leveraging Tax Credits and Deductions

Tax credits and deductions play a crucial role in tax reduction. Credits directly reduce the amount of tax owed, while deductions lower your taxable income. Common credits include the Child Tax Credit and the Earned Income Tax Credit. Firms also advise on deductions such as mortgage interest and medical expenses. They ensure you’re claiming everything you’re entitled to. The IRS provides detailed information on these credits and deductions.

Retirement Contributions

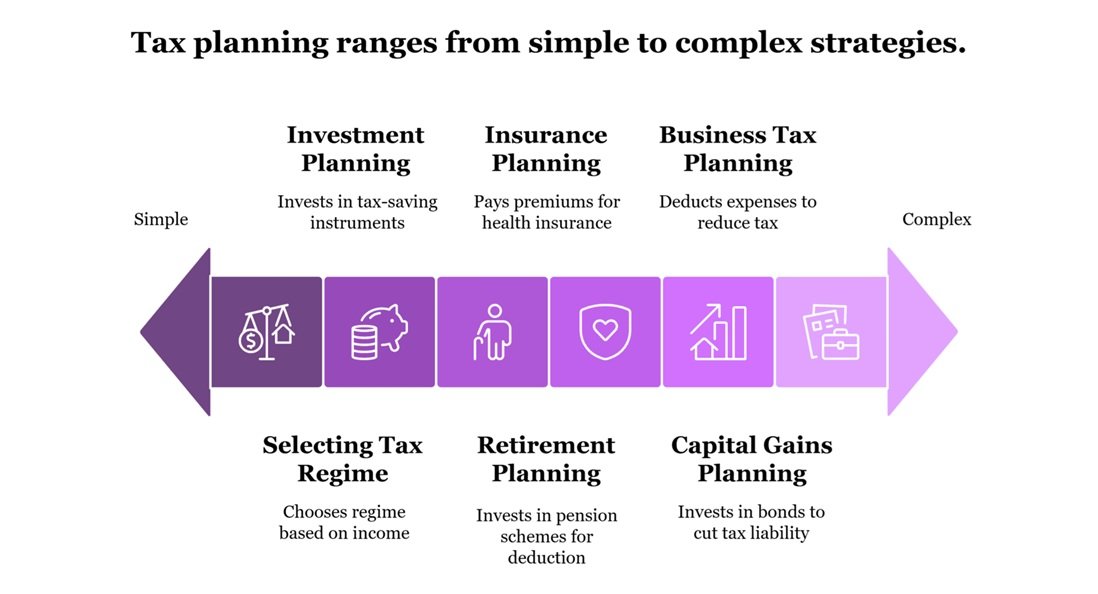

Contributing to retirement accounts can significantly lower tax liabilities. Traditional IRAs and 401(k)s reduce taxable income, leading to immediate tax savings. Roth IRAs, while not offering upfront deductions, grow tax-free. Additionally, employer-sponsored plans often include matching contributions, which add to savings. Consulting with a firm ensures you choose the best option for your financial goals.

Charitable Giving

Charitable donations not only help those in need but also provide tax benefits. By donating goods or cash, you can claim deductions that reduce taxable income. It’s important to keep records of donations for tax purposes. Firms can guide you through this process, ensuring compliance with IRS rules. Detailed guidelines are available on the IRS website.

Staying Informed About Tax Law Changes

Tax laws change frequently. Staying updated is crucial for optimizing tax strategies. Firms dedicate resources to track these changes. They ensure your tax plan adapts accordingly. This proactive approach keeps you compliant and maximizes your savings.

Comparing Tax Strategies

| Strategy | Advantages | Considerations |

|---|---|---|

| Income Deferral | Lowers current taxes | May not be suitable for all |

| Income Shifting | Reduces family tax burden | Requires careful planning |

| Retirement Contributions | Immediate deductions | Long-term commitment |

| Charitable Giving | Supports causes and offers deductions | Needs proper documentation |

Why Professional Help Matters

Working with tax professionals ensures you make the most of available strategies. They provide tailored advice that fits your unique situation. Professionals like those in Carmel, NY offer valuable insights. They help you navigate complex tax regulations with ease.

In conclusion, reducing tax liabilities is achievable with strategic planning. Firms assist by offering practical solutions tailored to your needs. Whether through credits, deductions, or retirement planning, every effort counts. Collaborate with experts to secure your financial future. Your proactive steps today pave the way for a more secure tomorrow.